Introduction: The Future of Biogas Has Arrived

For most of its history, biogas has existed quietly on the margins of the energy debate. A useful technology, certainly — but one that struggled to command the same attention as solar panels or wind turbines. That era is over.

In 2026, as the World Biogas Association (WBA) marks its tenth anniversary, the future of biogas is no longer a speculative question. It is a documented, data-backed, investment-grade reality.

More than 50 new biogas and biomethane policies have been introduced globally since 2020. Long-term industrial offtake agreements — deals that would have been almost unthinkable a decade ago — are now being signed between AD operators and some of the world’s largest corporations.

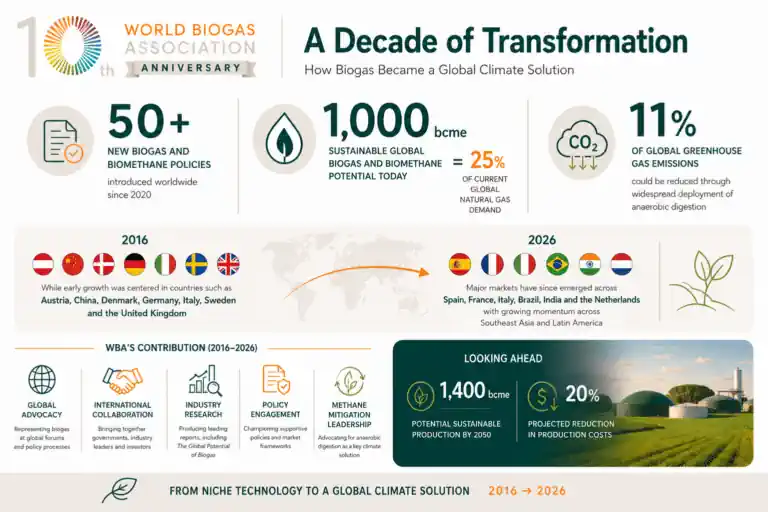

And the numbers at the heart of the WBA’s landmark anniversary report make an arresting case: sustainable global biogas production potential is estimated at nearly 1,000 billion cubic metres equivalent, equal to approximately 25% of current global natural gas demand.

This article explores what the future of biogas energy looks like in 2026 and beyond — who is driving it, where the growth is happening, what it means for climate action, and why the anaerobic digestion sector stands at what David Newman, Former President of the WBA, describes simply as “the beginning of its journey.”

We have included the full WBA anniversary press release below, followed by additional context and analysis for operators, investors, and policy-watchers who want to understand what these developments mean at ground level.

Key Takeaways

- The future of biogas is global, not just European. Major new markets have emerged across Spain, France, Brazil, India, and the Netherlands, with growing momentum in Southeast Asia and Latin America.

- Sustainable biogas production could meet 25% of current global natural gas demand — rising to the equivalent of nearly 1,400 bcme by 2050 as production costs fall by around 20%.

- Widespread anaerobic digestion deployment could reduce global greenhouse gas emissions by up to 11%, according to the WBA’s Global Potential of Biogas report.

- More than 50 new biogas and biomethane policies have been introduced globally since 2020, signalling a step-change in political recognition.

- Long-term industrial offtake deals — including Future Biogas’s 15-year agreement with AstraZeneca — mark biogas’s transition from subsidised niche to commercial mainstream.

- The WBA has launched the world’s first global certification scheme for biogas plants (ADCS International), underpinning the operational credibility the sector needs to attract institutional investment.

- For the UK AD sector specifically, the Simpler Waste Collection Strategy (due for implementation in 2026) is expected to unlock a significant new wave of food waste feedstock.

World Biogas Association 10th Anniversary Press Release

The following press release is reproduced in full and without alteration from the World Biogas Association, published 23 June 2026.

WBA PRESS RELEASE:

A Decade of Transformation: How Biogas Has Evolved from a Niche Technology to a Global Climate Solution

WBA celebrates its 10th anniversary in 2026, marking a decade that has seen biogas evolve into a globally recognised climate, energy, and circular economy solution.

Global momentum is growing, with 50+ new biogas and biomethane policies introduced since 2020 and major expansion across key international markets.

Biogas has the potential to meet 25% of current global natural gas demand and reduce up to 11% of global greenhouse gas emissions.

As the World Biogas Association (WBA) celebrates its 10th anniversary in 2026, the global biogas sector stands at a defining moment.

Ten years ago, biogas was largely concentrated in a handful of European markets. Today, it is increasingly recognised as a vital solution for climate action, methane mitigation, energy security, waste management, and circular economy development.

Since its founding in 2016, WBA has worked to elevate biogas on the international stage, bringing together policymakers, industry leaders and investors while advocating for supportive policies and greater recognition of the sector’s role in delivering net-zero ambitions.

The industry’s growth has accelerated significantly. According to the International Energy Agency (IEA), more than 50 new biogas and biomethane policies have been introduced globally since 2020.

While early growth was centred in countries such as Austria, China, Denmark, Germany, Italy, Sweden and the United Kingdom, major markets have since emerged across Spain, France, Italy, Brazil, India and the Netherlands, with growing momentum across Southeast Asia and Latin America.

The sector’s increasing maturity is evidenced by a growing number of long-term industrial offtake agreements, demonstrating increasing confidence in biomethane as a scalable, reliable and commercially viable energy solution. Recent examples include — Future Biogas’ 15-year agreement with AstraZeneca in the UK, Divert’s 10-year agreement with bp in the United States and growing compressed biogas (CBG) procurement agreements involving Indian public sector undertakings, including Indian Oil Corporation (IOC), Bharat Petroleum Corporation Limited (BPCL) and Hindustan Petroleum Corporation Limited (HPCL).

Today, sustainable global biogas and biomethane production potential is estimated at nearly 1,000 billion cubic meters equivalent (bcme) – equal to approximately 25% of current global natural gas demand. By 2050, this potential could rise to almost 1,400 bcme, while production costs are projected to fall by around 20%.

WBA’s landmark The Global Potential of Biogas report estimates that widespread deployment of anaerobic digestion could reduce global greenhouse gas emissions by up to 11%, demonstrating the sector’s potential to make a substantial contribution to climate mitigation efforts worldwide.

Reflecting on the industry’s progress, David Newman, Former President of the World Biogas Association, said:

“The many challenges humanity faces – from climate change and pollution to energy security and sustainable development – require global solutions. Biogas is one solution that can help humanity overcome several of these challenges, and I believe the industry is still at the beginning of its journey.”

He added:

“For biogas to grow and achieve international recognition, it requires an organisation that can represent the sector at global forums and advocate for its interests. WBA has fulfilled this role since its founding in 2016, and I am proud to have supported the organisation in its early years.”

Over the past decade, WBA has helped create the conditions for sector growth through global advocacy, policy engagement and international collaboration, ensuring biogas has a stronger voice in climate, energy and circular economy discussions worldwide.

Building on this foundation, WBA launched its #MakingBiogasHappen (MBH) programme to accelerate deployment through practical tools that support industry growth, including the Global Biogas Regulatory Framework (GBRF), which provides governments with a blueprint for developing successful biogas industries, and ADCS International, the world’s first global certification scheme for biogas plants, designed to drive operational excellence and build confidence across the sector.

As WBA enters its second decade, it remains focused on helping countries move from ambition to implementation and unlocking the full potential of biogas as a solution for climate action, energy security and sustainable development.

PR Ends

What Does the Future of Biogas Look Like at Ground Level?

The WBA’s headline figures are compelling, but what do they mean in practice — for operators, developers, and communities living alongside AD plants?

Larger Plants, More Feedstocks, Smarter Integration

The commercial model for biogas has changed significantly over the past decade and will continue to evolve. Early UK plants were relatively small, often co-located with a single farm or food processing site, and built primarily to generate electricity via combined heat and power (CHP) engines. The next generation of plants is larger, designed from the outset for biomethane grid injection, and drawing on blended feedstock streams — agricultural residues, food waste, sewage sludge, and industrial effluents — to maximise throughput and revenue stability.

In the UK, the Simpler Waste Collection Strategy, due for implementation in 2026, will mandate separate food waste collection from households and businesses across England. This is expected to unlock a significant increase in high-quality food waste feedstock available to AD operators — precisely the kind of development that could accelerate investment in new capacity and support the sector’s long-term growth trajectory.

For a deeper understanding of how anaerobic digestion works with different feedstocks and why it matters for the circular economy, see our comprehensive guide on anaerobic digestion and climate change.

Biogas and the Circular Economy

One aspect of biogas’s future that the WBA press release rightly highlights is its role beyond energy. Modern AD plants are increasingly being understood and operated as biorefineries — facilities that simultaneously produce renewable energy, recover nutrients, and return organic matter to the land in the form of digestate biofertiliser.

This circular economy dimension is becoming a competitive advantage as chemical fertiliser prices remain elevated and regulatory pressure on synthetic nitrogen increases. Digestate from well-managed AD plants can displace significant quantities of manufactured fertiliser, reducing a farm’s input costs and its embedded carbon footprint at the same time.

Biogas, in this framing, is not just a fuel — it is a cornerstone of a genuinely circular approach to organic waste. That makes its future resilience substantially greater than that of a single-purpose energy technology. Explore this angle further in our post on decarbonisation strategies using renewable energy from biogas.

The Methane Emissions Reduction Opportunity

One of the most under-appreciated aspects of biogas’s future potential is its role in reducing fugitive methane emissions — not just in replacing fossil fuels. Methane is approximately 80 times more potent than CO₂ as a greenhouse gas over a 20-year period. Organic waste decomposing in landfills, manure sitting in open lagoons, and food residues in open compost heaps all release methane directly into the atmosphere.

Anaerobic digestion captures that methane before it escapes, converts it into a usable energy carrier, and in doing so delivers a double climate dividend: less methane in the atmosphere, and less fossil fuel combusted elsewhere. This is why the WBA’s estimate that AD could reduce global GHG emissions by up to 11% is, if anything, conservative — it does not fully account for all the methane capture scenarios that are technically feasible.

For a detailed look at this dimension of biogas’s climate potential, see our article on the role of biogas in methane emissions reduction.

Biogas and Biomethane: The Policy Landscape Shaping the Future

Europe: From Feed-in Tariffs to Market Integration

European biogas policy has gone through several distinct phases. The early growth model relied heavily on feed-in tariffs — guaranteed prices for electricity from biogas CHP plants — particularly in Germany and the UK. As those tariff regimes matured or closed, the sector pivoted toward biomethane grid injection, supported by mechanisms such as the UK’s Green Gas Support Scheme (GGSS) and the EU’s REPowerEU biomethane targets.

The EU has set a target of 35 billion cubic metres of biomethane production per year by 2030 — a five-fold increase on current levels. Achieving this will require sustained policy support, streamlined grid connection regulations, and continued investment in upgrading capacity. The European Biogas Association’s Grid Ready Forum, convened in Brussels in April 2026, flagged that regulatory fragmentation between member states remains one of the most significant barriers to hitting that target.

The UK: Ambitious Targets, Evolving Support

In the UK, the Green Gas Support Scheme has been extended to 2028, maintaining tariff support for new biomethane injection projects. The government’s Biomass Strategy identifies a target of 30–40 TWh of biomethane per year — compared to around 7 TWh currently being injected — underlining the scale of expansion the sector is expected to achieve.

For an in-depth look at the UK policy outlook for biogas and biomethane, including the GGSS, RTFO, and what the sector needs from government in the years ahead, see our article on biogas and biomethane — the future of renewable energy in the UK.

Emerging Markets: India, Brazil, and Southeast Asia

Perhaps the most significant development highlighted in the WBA’s anniversary assessment is the globalisation of biogas. For the first decade of significant growth, the technology was essentially European — with Germany, the UK, Denmark, and Italy accounting for the lion’s share of installed capacity.

That geography is changing fast. India’s compressed biogas (CBG) programme — backed by procurement agreements with Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum — represents one of the most ambitious government-led biogas expansion programmes in the world. Brazil’s enormous agricultural sector and organic waste streams give it some of the highest biogas production potential of any country outside Europe. And Southeast Asia’s rapidly growing urban populations and expanding food processing industries create feedstock opportunities at scale.

The future of biogas is genuinely global — and that globalisation opens up new markets, new supply chains, and new investment opportunities for technology developers, engineering firms, and equipment suppliers based in established markets like the UK.

The Investment Case for Biogas in 2026

Long-term industrial offtake agreements are not just operationally important — they are a signal to the capital markets. When AstraZeneca signs a 15-year biomethane supply agreement with Future Biogas, it is not simply buying renewable energy. It is providing the revenue certainty that makes project financing bankable at competitive rates.

This matters enormously for the future pace of biogas development. AD plants have relatively high upfront capital costs and long operational lives. Historically, the difficulty of securing long-term revenue certainty — outside of government tariff schemes — was a significant constraint on investment. Corporate power purchase agreements (PPAs) and gas offtake deals are beginning to fill that gap, making biogas investment attractive to a broader pool of institutional capital.

The IEA forecasts that green gas will grow at approximately 15% annually until 2035 and 8.9% annually to 2050 if net-zero targets are to be met — growth rates that significantly exceed the average for renewables overall. For investors with a long time horizon, the fundamentals of the biogas sector look increasingly compelling.

For an overview of current biomethane pricing and what it means for project economics, see our detailed 2026 analysis on biomethane as a natural gas replacement and what factors are shaping the market.

The Role of ADCS International and Global Certification

One of the practical tools the WBA has developed to support the sector’s long-term credibility is ADCS International — described as the world’s first global certification scheme for biogas plants. This is a significant development that deserves more attention than it typically receives.

Certification schemes matter for several reasons. They provide independent assurance to offtake partners, lenders, and insurers that a plant is being operated to defined standards. They create a common benchmark that makes cross-border comparison and investment easier. And they underpin the integrity of biomethane’s environmental claims — an increasingly important consideration as corporate buyers face scrutiny over the rigour of their green energy purchasing.

For operators of UK and European AD plants, ADCS International certification is worth tracking closely. As the market for verified, certificated biomethane matures, plants without recognised operational accreditation may find it harder to access premium offtake agreements or favourable financing terms.

Conclusion: Why the Future of Biogas Is More Certain Than Ever

Ten years ago, describing biogas as a “global climate solution” would have required a significant leap of faith. Today, the evidence is compelling enough that even cautious institutional investors are beginning to take notice.

The WBA’s tenth anniversary assessment does not claim that biogas will single-handedly solve climate change. What it demonstrates — with data, with policy precedent, and with commercial track record — is that the future of biogas energy is larger, more geographically distributed, and more commercially mature than almost anyone predicted when the sector first began to scale.

The 25% of global gas demand figure is not a utopian aspiration. It is a technically grounded estimate of what is achievable with the right policy frameworks, investment levels, and feedstock mobilisation. The 11% reduction in global greenhouse gas emissions is similarly grounded in analysis of what AD deployment could achieve if fully exploited across waste, agriculture, and industry.

For anyone working in, investing in, or thinking about the anaerobic digestion sector, the message from the WBA’s first decade is straightforward: the technology works, the market is growing, and the beginning — as David Newman rightly says — is exactly where we are.

To explore more about how biogas works, what it can do for your business or community, and how to get involved in the sector, start with the reason biogas production is so worthwhile and read our posts on anaerobic digestion and climate change and biogas versus natural gas — the environmental comparison.

You may also like to read:

- Environmental benefits and disadvantages of AD for anaerobic wastewater treatment → Because AD does have some disadvantages.

Frequently Asked Questions

What is the future of biogas energy?

The future of biogas energy is one of sustained global growth. The World Biogas Association estimates that sustainable production potential could meet around 25% of current global natural gas demand, rising toward nearly 1,400 billion cubic metres equivalent by 2050. Growth is increasingly global, with major new markets emerging in India, Brazil, Spain, and Southeast Asia alongside the established European leaders.

Can biogas replace natural gas?

Biogas — once upgraded to biomethane — is chemically identical to natural gas and can be injected directly into existing gas grids with no infrastructure modification. While it is unlikely to replace 100% of natural gas demand in the near term, it can realistically substitute a significant proportion, particularly in hard-to-electrify sectors such as heavy industry, maritime transport, and high-temperature process heat.

How much can biogas reduce greenhouse gas emissions?

The WBA’s Global Potential of Biogas report estimates that widespread deployment of anaerobic digestion could reduce global greenhouse gas emissions by up to 11%. This figure reflects both the displacement of fossil fuels and the capture of fugitive methane that would otherwise be released from organic waste in landfill, slurry lagoons, and open compost.

What is driving biogas growth in 2026?

Key drivers include the proliferation of government support policies (50+ new policies since 2020 according to the IEA), the emergence of long-term corporate offtake agreements providing revenue certainty, falling production costs, and the globalisation of the market beyond its traditional European base. The EU’s REPowerEU biomethane target of 35 billion cubic metres per year by 2030 is also a major accelerant.

What is ADCS International?

ADCS International is the world’s first global certification scheme for biogas plants, developed by the World Biogas Association. It is designed to drive operational excellence, provide independent assurance to offtake partners and lenders, and build confidence in the sector’s environmental claims. It is an increasingly important credential for operators seeking to access premium commercial agreements.

Is biogas a good investment in 2026?

The investment case for biogas has strengthened significantly. The IEA projects green gas growth of around 15% per year to 2035. Long-term corporate offtake deals are making project finance more accessible at competitive rates. And the combination of energy revenues, gate fees for waste treatment, and digestate sales creates a diversified income model that compares favourably with single-revenue renewable technologies. As with any capital-intensive infrastructure investment, project-level due diligence on feedstock, grid connection, and policy risk remains essential.

Where can I learn more about biogas and anaerobic digestion?

Our main site at anaerobic-digestion.com covers the full range of AD technologies, applications, and policy developments. For more on the specific topics covered in this article, see our posts on biomethane advantages and disadvantages, innovative biogas projects in renewable energy, and biogas generators — the future of waste to energy.

You might also like to read “Biomethane as a Natural Gas Replacement: How Close Are We?”

Sources: World Biogas Association (WBA) 10th Anniversary Press Release, June 2026; IEA Biogas and Biomethane Policy Tracker; Oxford Institute for Energy Studies NG203 (January 2026); European Biogas Association Grid Ready Forum (April 2026); UK Biomass Strategy 2023; Xoserve Decarbonisation Knowledge Centre.