The UK's first claimed example of the new breed of unsubsidised biomethane plants is Moor Bioenergy in Lincolnshire. It was commissioned by Future Biogas and AstraZeneca in Feb 2025. This facility demonstrates the commercial viability of green gas without taxpayer support through long-term corporate power purchase agreements (CPPAs) and integrated carbon capture.

Quick Overview: The Role of Circular Economics in Biomethane's Future

- Unsubsidised biomethane plants can become financially viable when they stop treating digestate and biogenic CO2 as waste and start treating them as sources of income.

- Studies indicate that the likelihood of a biomethane plant achieving a positive net present value (NPV) ranges from a mere 1% to 59%, depending on the type of feedstock and subsidy conditions. This wide range calls for a more intelligent financial model.

- Anaerobic digestion produces three commercially valuable by-products: biomethane, digestate biofertiliser, and biogenic CO2. However, most plants are only making money from one of these.

- The circular economics model combines all three revenue streams, fundamentally altering the financial argument for plants that operate without government incentives.

- Unsubsidised biomethane is already being injected into the existing gas grid, demonstrating that operating without subsidies is not a future concept, but a current reality.

Most biomethane plants are missing out on significant potential revenue, and subsidies are partially responsible for obscuring this issue.

When the gap between production costs and market revenue is covered by government incentive tariffs, there's not much pressure to optimise every output stream. However, as subsidy frameworks change and policy support becomes less certain, the plants that will survive – and thrive – are those built from the ground up around circular economics.

Future Biogas, one of the UK's leading anaerobic digestion operators, is already showing that delivering unsubsidized biomethane through the gas grid is not only possible, but operational.

Hidden Revenue Opportunities for Unsubsidised Biomethane Plants

The main issue is a matter of perception. Biomethane has traditionally been seen as a one-product industry – organic feedstock goes in, renewable gas comes out, and it's sold. Everything else, including the digestate, the separated CO2, and the residual heat, is considered a byproduct at best and a disposal cost at worst.

This mindset is costly. For unsubsidised biomethane plants to be viable, the biogas industry must invest more and create multiple income streams.

Three unique and commercially viable products are produced by a fully circular anaerobic digestion plant. Each of these products has a market that it can address. Each of these products contributes to the revenue stack that determines whether a plant's net present value turns positive without needing a subsidy cheque to fill the gap. The plants that understand this architecture are the ones that are rewriting the definition of financial viability for this sector.

Understanding the 3 Main Products of Anaerobic Digestion

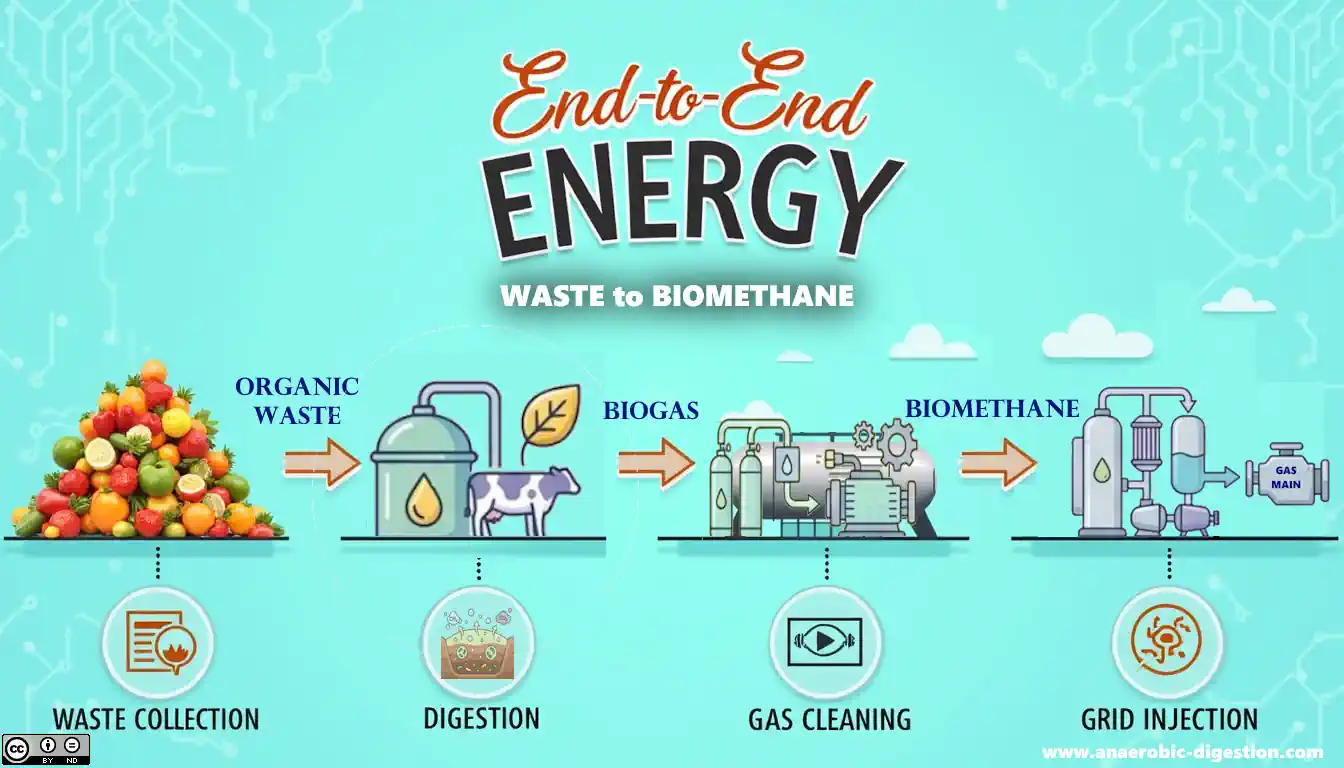

Anaerobic digestion is a process that occurs naturally, where organic feedstock like crops, food waste, animal manure, and sewage sludge are broken down by micro-organisms in an environment without oxygen.

As these micro-organisms do their job, they produce biogas. This biogas is then cleaned and upgraded to separate it into its individual components. The end result of this process is not a single product, but three.

1. Biogas: The Main Product Everyone is Familiar With

The main components of raw biogas are methane (CH4) and carbon dioxide (CO2), with minor amounts of trace gases such as hydrogen sulphide (H2S) and water vapour. After upgrading — which involves removing the CO2, H2S, and water vapour — what is left is biomethane. This renewable gas is chemically the same as fossil natural gas, but it is carbon-negative over its lifecycle when it comes from sustainable feedstocks.

This is the product that gets injected into the gas grid, sold to industrial off-takers, or used to fuel green transport. It's the headline output, and it absolutely matters. But it's only one-third of the value equation.

2. Why We Shouldn't Ignore Digestate: A Natural Fertiliser

Once the anaerobic digestion process is finished, a residue rich in nutrients is left behind in the digester. This is what we call digestate — a potent natural biofertiliser that contains nitrogen, phosphorus, and potassium in forms that plants can easily absorb. Farmers who use digestate on their land are effectively reducing their need for synthetic fertilisers. Given the recent Russia-Ukraine conflict and the resulting instability in fertiliser prices, this reduction can translate into significant monetary savings.

Nonetheless, the value of digestate is often underestimated in plant business models. Some operators view it as a logistical problem rather than a commercial opportunity. This is a significant oversight – one that the circular economics model rectifies by giving digestate the rightful place it deserves in the revenue structure.

3. Carbon Capture: A Unique Opportunity

CO2 is physically separated from the methane stream during the biogas upgrading process. In a traditional plant, this CO2, which is biogenic, is vented to the atmosphere — effectively throwing away a product that food manufacturers, beverage producers, greenhouse horticulturalists, and industrial gas suppliers are willing to pay for.

This stream, when paired with carbon capture technology, turns from an emission into an additional revenue line. When the CO2 is captured rather than released, and the biomethane is derived from sustainable feedstocks, the entire system can become carbon-negative.

Why Biomethane Can't Rely on Subsidies Forever

Subsidies played a crucial role in scaling up biomethane to a commercial level. Without them, the initial economic model just wasn't viable.

But the very incentives that spurred growth have also made the sector dependent on them — a problem that becomes glaringly obvious the moment the subsidy conditions change.

The Financial Instability Caused by Dependence on Subsidies

If a plant's revenue relies on a particular subsidy rate, any alteration to that rate can have a domino effect on the plant's entire financial model. The risks of policy reviews, tariff reduction timetables, and shifting political priorities are not merely theoretical — they are proven aspects of every major biomethane incentive program that has ever been implemented.

The Renewable Heat Incentive (RHI) in the UK is a prime example. When the future of the scheme became uncertain, plants that were built around the assumptions of RHI tariffs had to undergo major recalculations. Operators who had invested in things like feedstock supply chains, grid connection infrastructure, and processing capacity found themselves in a vulnerable position because their investments were based on revenue projections that included subsidies.

This is not to say that subsidies are a bad policy tool. They are effective. However, there is a significant difference between designing a plant that needs subsidies to stay afloat and designing a plant that gains from subsidies but can still operate without them. This difference is crucial when it comes to the security of long-term investments.

Small plants are where the vulnerability is most evident. Studies into small- and medium-sized biomethane facilities that use the organic fraction of municipal solid waste (OFMSW) as feedstock illustrate just how unstable the economics of subsidy reliance can be. The financial results of models that rely on subsidies can vary widely based on:

- The specific incentive tariff applied and its duration

- Feedstock type and availability (OFMSW versus agricultural by-products versus energy crops)

- Plant scale — capital costs don't scale linearly, creating size-dependent risk profiles

- Local gate fees and tipping charges associated with waste feedstock intake

- Biomethane spot prices and long-term offtake contract terms

What Happens When Incentive Tariffs Don't Cover Plant Costs

- Operating cash flows turn negative, forcing operators to draw down reserves or seek refinancing

- Feedstock supply contracts become difficult to honour if tip fees were subsidising intake volumes

- Grid injection agreements may include minimum volume clauses that become operationally unviable

The cascading effect of tariff shortfall is rarely limited to a single balance sheet line. When incentive income drops below the threshold needed to service debt and cover operating expenditure simultaneously, operators face a compounding problem: they cannot reduce fixed costs quickly enough to match reduced revenue, and variable cost reductions — such as cutting feedstock intake — directly reduce the biomethane output they need to sell.

Plants that have reached this point have either stopped operating, sought emergency refinancing, or switched to alternative feedstocks in the middle of a contract in documented cases, each option carrying high financial and reputational costs. The lesson is structural: a plant designed to be viable only with subsidies is not a viable plant. It is a subsidised project with a renewable energy output.

Don't mistake this for a negative outlook on biomethane. It's quite the contrary. This is a case for constructing these facilities properly right out of the gate, using a business model that relies on several revenue streams and doesn't fall apart when policy environments change.

The NPV Issue: Why 1–59% Profitability Chances Are Not Enough

Academic research on biomethane plant profitability paints a grim picture. Studies published in peer-reviewed journals on incentive policies in biomethane production show that the likelihood of achieving a net present value greater than zero — the basic threshold for a project to be financially viable — ranges from as low as 1% to as high as 59% when using OFMSW as feedstock. This is a huge range and it demonstrates how sensitive these projects are to the factors working against them under single-output business models.

A project with a 1% chance of NPV > 0 is not viable. It's a gamble with infrastructure costs. Even at 59%, a responsible developer or lender should be deeply uncomfortable committing capital to a project with a 41% chance of losing value. These numbers are not arguments against biomethane — they are arguments against the financial structure that produces them. The circular economics model exists precisely to improve those odds.

Commercialising Digestate Alters the Financial Equation

When digestate is given its rightful commercial worth, the economic model for a biomethane plant is radically transformed.

This isn't a small enhancement — it's a foundational shift in revenue calculation, cost offsetting, and how the overall project NPV is presented to investors and lenders.

Why Digestate is a Premium Biofertiliser

It's important to note that digestate isn't your everyday compost. It's a rich organic fertiliser packed with nitrogen (N), phosphorus (P), and potassium (K) that plants can immediately utilise. The nitrogen in digestate is primarily ammoniacal nitrogen, the same type found in synthetic fertilisers like ammonium nitrate. This means it can deliver agricultural results that are on par with factory-made alternatives, minus the fossil fuel cost associated with their production.

The composition and quality of digestate are influenced by the type of feedstock that was used in the digester. Digestate from food waste is usually very high in nitrogen. Digestate from energy crops usually has a balanced NPK profile that is suitable for broad-acre arable applications.

Operators who certify their digestate to recognised standards, like the PAS 110 specification in the UK, can sell it at significantly higher prices than those who sell it uncertified as a generic soil conditioner.

How Digestate Replaces Synthetic Fertiliser Expenses on Farms

For farms that receive digestate — whether it's the same farm providing the feedstock or nearby farming operations — the financial argument is straightforward and quantifiable. Every tonne of certified digestate used on a field is a tonne of synthetic fertiliser that doesn't need to be bought. During times of high fertiliser prices, like the ones seen across European markets after supply disturbances in 2021 and 2022, this displacement value can be significant.

For those operating biomethane plants and providing their own feedstock from farming activities on-site, digestate provides a real closed loop: organic matter goes in, renewable gas and fertiliser are produced, and the fertiliser is reapplied to the land that grew the feedstock.

The cost of crop production is reduced. The economics of the entire system are enhanced. This is a perfect example of circular economics — value is circulated through the system rather than being lost.

Completing the Nutrient Cycle: The Real-World Application of Circular Economics

Traditional agricultural practices follow a linear model, depleting nutrients from the soil through crop production, replacing them with energy-intensive, artificially produced fertilisers, and creating organic waste during processing that is often disposed of in landfills or incinerators.

The use of anaerobic digestion with digestate return disrupts each of these steps. Organic waste is transformed into feedstock, which is then used to produce energy and fertiliser. The fertiliser is returned to the soil, completing the nutrient cycle. This is not just a theoretical idea of sustainability – it results in a quantifiable reduction in costs across the system, directly enhancing the economics of the plant.

CO2 Capture Converts Waste into Profit

Biogenic CO2, one of the three byproducts of anaerobic digestion, is often overlooked. As part of the biogas upgrading process, CO2 is physically separated from methane to produce biomethane that meets grid standards.

Unfortunately, most plants simply release this CO2 into the air. This is a missed opportunity, as CO2 can be a valuable resource under the right market conditions.

It's important to understand the difference between biogenic CO2 and fossil CO2. Biogenic CO2 comes from organic material that has recently absorbed carbon from the atmosphere through photosynthesis.

When it is released – whether through burning, digestion, or venting – it is returning carbon to the cycle it came from, rather than adding new fossil carbon to the atmosphere. This makes it not just acceptable, but often preferable, to fossil-derived CO2 for industrial buyers who are operating under carbon accounting frameworks.

There is a real and expanding market for captured biogenic CO2, and it is currently under-supplied compared to potential demand. Food and beverage manufacturers, greenhouse growers, and industrial gas distributors are all active buyers.

For a biomethane plant that has already paid the capital cost of an upgrading unit to separate CO2 from methane, adding a liquefaction or compression system to capture and sell that CO2 rather than vent it represents one of the highest-return incremental investments available in the sector.

How Biomethane Upgrading Separates Biogenic CO2

Standard upgrading technologies — pressure swing adsorption (PSA), water scrubbing, and membrane separation — all create a CO2-heavy off-gas stream as a direct result of the separation process.

In a traditional plant configuration, this stream is sent to a vent stack. In a circular plant configuration, it is sent to a capture and purification unit where it is compressed, dried, and either liquefied for bulk transport or stored in pressurised cylinders for direct industrial supply.

When properly purified, the CO2 produced is usually food-grade quality, which opens up the highest-value end of the buyer market.

Who Buys Captured Biogenic CO2?

There are many industries that need food-grade and industrial biogenic CO2 for their operations.

Carbonated beverage makers need CO2 to create the fizz in their soft drinks and beers.

Greenhouse horticulturalists use CO2 to speed up plant growth. This is especially true in large-scale tomato and cucumber production.

Meat processors use CO2 in modified atmosphere packaging to make their products last longer.

Dry ice makers turn liquid CO2 into a solid for cold chain logistics. All of these industries are stable, recurring buyers of a product that most biomethane plants are currently giving away for free.

How the Circular Model Makes Biomethane Plants Profitable Without Subsidies

Once the three revenue streams are correctly factored in, the financial reasoning is simple. A plant that only sells biomethane is dependent on a single price signal in one market. A plant that sells biomethane, certified digestate, and captured biogenic CO2 has three separate revenue lines. Each line has its own market dynamics and provides a certain amount of natural protection against price changes in the others.

By diversifying revenue streams in unsubsidised biomethane plants, the total income increases, and the risk profile of the project changes. Lenders see a fundamentally different credit proposition when they assess a biomethane project with three separate, contracted revenue streams compared to a single-output plant that depends on spot gas prices and policy continuity. The cost of capital improves. The debt service coverage ratio improves. The overall project viability improves — often without any change to the underlying physical infrastructure beyond the addition of CO2 capture equipment and digestate certification processes.

The type of feedstock used is still incredibly important. Plants that use OFMSW can receive gate fees, which are payments for accepting the waste. This provides a fourth source of revenue before any biomethane has even been produced. Agricultural by-products and energy crops that are grown for this specific purpose each have different costs and yields, which can affect the final NPV of the circular model. However, regardless of the type of feedstock used, the effect of adding revenue from digestate and CO2 is the same: it significantly increases the likelihood of a positive NPV. Learn more about the benefits of biomethane in green energy.

Profit Structure: Biomethane, Digestate, and CO2 Together

The profit structure of completely circular, unsubsidised biomethane plants looks something like this:

| Revenue Stream | Source | Market | Value Driver |

|---|---|---|---|

| Biomethane (CH4) | Upgraded biogas | Gas grid / industrial offtake | Renewable gas price, carbon intensity value |

| Digestate biofertiliser | Post-digestion residue | Agricultural sector | Synthetic fertiliser displacement value |

| Biogenic CO2 | Upgrading off-gas | Food, beverage, horticulture | Food-grade CO2 market price |

| Gate fees (waste feedstock) | OFMSW / food waste intake | Waste management sector | Tipping fee per tonne of waste received |

When all four streams are active simultaneously, the financial model stops looking like a renewable energy project propped up by policy and starts looking like a diversified circular resource business that happens to produce renewable energy as its primary output. That reframing is not cosmetic — it changes how the project is financed, how it is valued, and how resilient it is to external shocks.

Plant Size and Feedstock Type Remain Critical

Not all circular biomethane plants will achieve the same NPV results, and the choice of feedstock remains one of the most critical decisions in plant design.

OFMSW-fed plants benefit from gate fees that immediately offset operating costs before any product is sold, but they face more complex feedstock quality management and regulatory compliance requirements.

Agricultural by-product plants tend to have a more predictable feedstock composition and a lower risk of contamination, but they do not receive tipping fees.

Energy crop-fed plants offer consistent gas yields but carry the input cost of growing the crop itself. The circular model improves economics across all three categories — but the starting point differs, and plant sizing must reflect that.

The size of the plant also plays a significant role in ways that may not be immediately apparent. The capital costs associated with upgrading equipment, CO2 capture systems, and digestate processing infrastructure do not scale linearly with the capacity of the plant.

A medium-sized plant may be able to reach the economic threshold for investment in CO2 liquefaction more efficiently than a smaller plant, while a larger plant may generate volumes of digestate that require a dedicated logistics infrastructure in order to effectively monetise.

It is just as important to match the size of the plant to the revenue stack as it is to get the feedstock right.

Unsubsidised Biomethane Plants are Already Delivering Green Gas Through the Gas Grid

This isn't just a theory. Future Biogas has announced that it is already delivering unsubsidised biomethane through the existing UK gas grid to meet commercial gas demand. They are developing new fully additional anaerobic digesters with carbon capture to meet this demand, with green gas balanced through the grid.

The fact that this is already operational, at a commercial scale, without subsidy support, is the most important fact in the entire debate about the viability of biomethane.

It shows that applying circular economics to anaerobic digestion results in a financially viable business, not just a financially plausible model.

The Future Standard of Biomethane Plants is Circular, Not the Exception

The energy transition doesn't wait for the ideal conditions. The biomethane plants that will still be in operation in twenty years are the ones that are being designed today based on circular economics

— plants that view every output as a source of revenue,

- that close nutrient cycles,

- that capture carbon instead of releasing it, and

- that incorporate financial resilience into their structure rather than relying on policy frameworks.

Subsidies will continue to be a factor in speeding up deployment, but they will not determine viability. Circular economics will. The sector already has a proof of concept. What it needs now is a broader adoption of the model that makes it possible.

Commonly Asked Questions – Re: Unsubsidised Biomethane Plants

The economics of biomethane plants can seem complicated, but the main questions are simple. Here are the responses to the most frequently asked questions about the feasibility of circular biomethane.

What is digestate and why is it commercially valuable?

Digestate is the nutrient-rich byproduct of anaerobic digestion. It contains nitrogen, phosphorus, and potassium in forms that plants can use — the same essential nutrients found in synthetic fertilisers. Its commercial value comes from its ability to replace synthetic fertilisers on farmland.

When certified to standards like PAS 110 in the UK, digestate can be sold as a certified biofertiliser product rather than simply used as a generic soil conditioner, which significantly increases the price it can fetch in the market.

For operators of biomethane plants, digestate is not a waste product — it is a source of revenue that increases with better management of feedstock and quality certification.

How can capturing CO2 make a biomethane plant more profitable?

As part of the biogas upgrading process, CO2 must be physically separated from methane. In most plants, this CO2 is simply released into the atmosphere, which means a potentially valuable gas is being wasted. By installing a system that captures, purifies, and compresses this CO2, it can be turned into a product that can be sold.

Food-grade biogenic CO2 is used by manufacturers of carbonated drinks, greenhouse horticulturists, meat packers who use modified atmosphere packaging, and dry ice manufacturers.

Adding CO2 capture to an existing unsubsidised biomethane plant upgrading unit is a cost-effective method because the capital cost is significantly lower than the cost of the upgrading unit. This means that the return on the additional investment is usually high. Moreover, it provides a third independent revenue stream to the plant, which reduces the overall financial risk from changes in any single market, including the biomethane gas price.

Is it possible for a biomethane plant to function without the support of government subsidies?

It is possible, and it is already taking place. The crucial requirement is that the plant must be constructed with multiple sources of revenue in mind, rather than just the price of biomethane. A plant that relies solely on the revenue from biomethane requires either a very high gas price or a subsidy to cover the difference between the cost of production and the return on the market.

A plant that also makes money from digestate and captured CO2, and may also receive gate fees for waste feedstock, has a fundamentally different cost-to-revenue relationship.

When all streams are active and contracted, the NPV calculation changes enough to make operation without subsidies not only possible, but commercially sensible. Future Biogas is currently delivering unsubsidised biomethane through the UK gas grid, which is the most tangible evidence that this model works in practice.

How does biogenic CO2 differ from fossil CO2?

The two forms of CO2 differ in their source, which in turn affects how they are accounted for in climate and sustainability frameworks. To understand more about the impact of biogenic CO2, consider exploring the link between water, soil, and successful anaerobic projects.

Characteristic Biogenic CO2 Fossil CO2 Carbon origin Recently atmospheric — absorbed by plants through photosynthesis Ancient — locked underground for millions of years Carbon cycle impact Returns existing atmospheric carbon to the cycle Adds new carbon to the active atmospheric cycle Climate accounting Carbon-neutral to carbon-negative (with capture) Carbon-positive — increases atmospheric CO2 concentration Industrial acceptability Preferred by buyers under carbon accounting frameworks Carries embedded carbon cost under emissions reporting Source in biomethane context Separated during biogas upgrading from organic feedstock Not applicable — biomethane process produces biogenic CO2 only

Biogenic CO2 from a biomethane upgrading unit is chemically identical to fossil CO2 — the same molecule, the same industrial properties, the same applications. The difference is entirely in its origin and what that means for the carbon accounting of whoever buys and uses it.

For industrial buyers operating under Scope 3 emissions reporting requirements, substituting fossil-derived CO2 with biogenic CO2 can directly reduce their reported emissions intensity. That preference is driving increasing demand for certified biogenic CO2 supply, making it progressively more valuable as a commercial product.

Producing biomethane from renewable feedstocks in unsubsidised biomethane plants and capturing the biogenic CO2 instead of releasing it can make the entire production system carbon-negative. This means it takes more carbon out of the active atmospheric cycle than it puts in. This is an important distinction in a market where corporate buyers are willing to pay more for truly carbon-negative energy.

How is circular economics used in anaerobic digestion?

In anaerobic digestion, circular economics is about designing a system where everything produced is used, sold, and valued. It also means that the products of one part of the system are used in another part. Nothing is wasted. Nothing is thrown away, put in a landfill, or considered a disposal cost when it could be sold or reused.

Essentially, this indicates that the organic material put into the digester comes from waste streams that would otherwise require disposal, thus completing a cycle in the waste management system. The biomethane produced replaces fossil gas in the energy system, thus completing a cycle in the carbon cycle.

The digestate returns nutrients to agricultural land, thus completing the nutrient cycle that synthetic fertiliser manufacturing currently disrupts. The captured CO2 provides industrial buyers who would otherwise source fossil-derived CO2, thus completing another cycle in the carbon economy.

Every closed loop creates value. Each one cuts a cost somewhere in the system — whether directly for the plant operator, or for the buyer who gets a lower-carbon input. This combined value is what makes circular anaerobic digestion economically better than the linear single-output model, and it's what makes unsubsidised viability a reality rather than a dream.

The success of biomethane isn't tied to waiting for improved subsidies or increased gas prices. It is about constructing unsubsidised biomethane plants that produce value from every process output, close every accessible resource loop, and incorporate financial resilience into the system's architecture.

That is the promise of circular economics — and it is already delivering. To understand what commercial-scale biomethane supply without subsidies looks like, Future Biogas is currently developing and managing these types of projects across the UK. For more insights, explore the importance of anaerobic digestion for food manufacturers.